Startups in Japan raised a total of JPY 779.3 billion (excluding debt financing) in 2024, remaining relatively stable at +3% YoY. At the same time, a string of large deals worth over JPY 5 billion in the second half of the year contributed to a rise in the average value of individual deals. It is also worth noting that 2024 saw an increase in investment activity from prominent foreign investors, with leading global VCs such as Khosla Ventures and New Enterprise Associates showing interest in the Japanese market.

Although Japan’s investment landscape showed signs of a shift, with the number of startup funds established decreasing significantly YoY, general business corporations continued to be engaged in different ways—including in the form of corporate venture capital funds (CVCs)—and M&A activity was high.

“Japan Startup Funding” is a biannual report published by Speeda, a leading platform for economic information in Japan, presenting the latest trends in startup funding in the country based on original research and analysis. Recognized as the gold standard for information on Japan’s startup industry, it has been cited in national policies such as the Startup Development Five-Year Plan and other materials produced by Japan’s Ministry of Economy, Trade and Industry.

This is an English version of the preliminary report prepared as a summary in advance of the release of the full “Japan Startup Funding report for 2024” (full report available in Japanese only).

CONTENTS

Overall Funding Stable

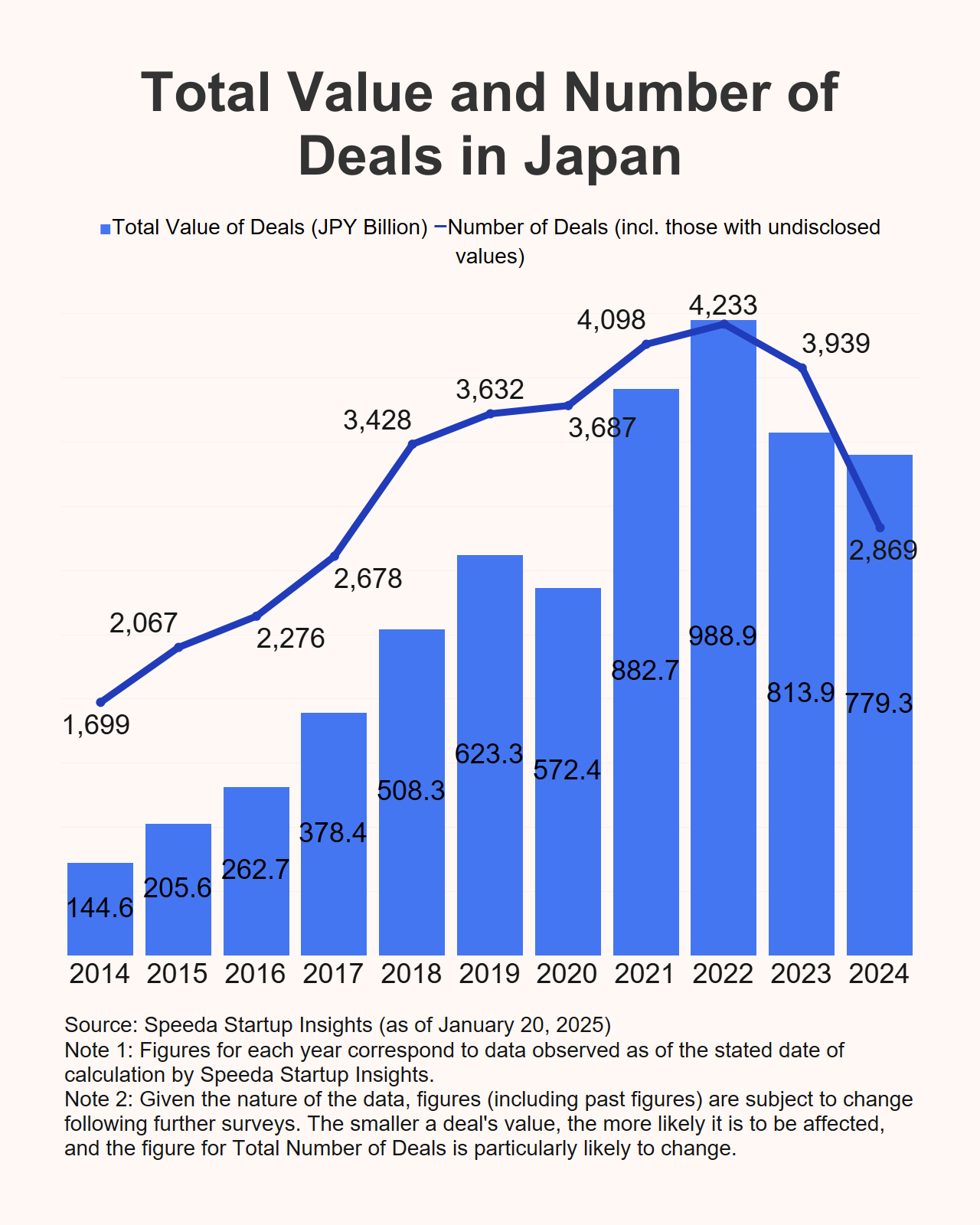

Startup funding in Japan was firm in 2024, with startups securing JPY 779.3 billion (excluding debt financing) in total investments—a 3% YoY increase over the JPY 753.6 billion raised in 2023. At the same time, the average value of individual deals was JPY 310 million, surpassing the JPY 250 million recorded in 2023. Nonetheless, even when taking into account deals that have yet to be disclosed, total startup funding in Japan is likely to have fallen short of the amount raised in 2021.

Meanwhile, the number of startups that received funding (i.e., the total number of deals) in 2024 actually saw a marginal YoY increase from 2,828 to 2,869.

Major Funding Rounds Concentrated in H2

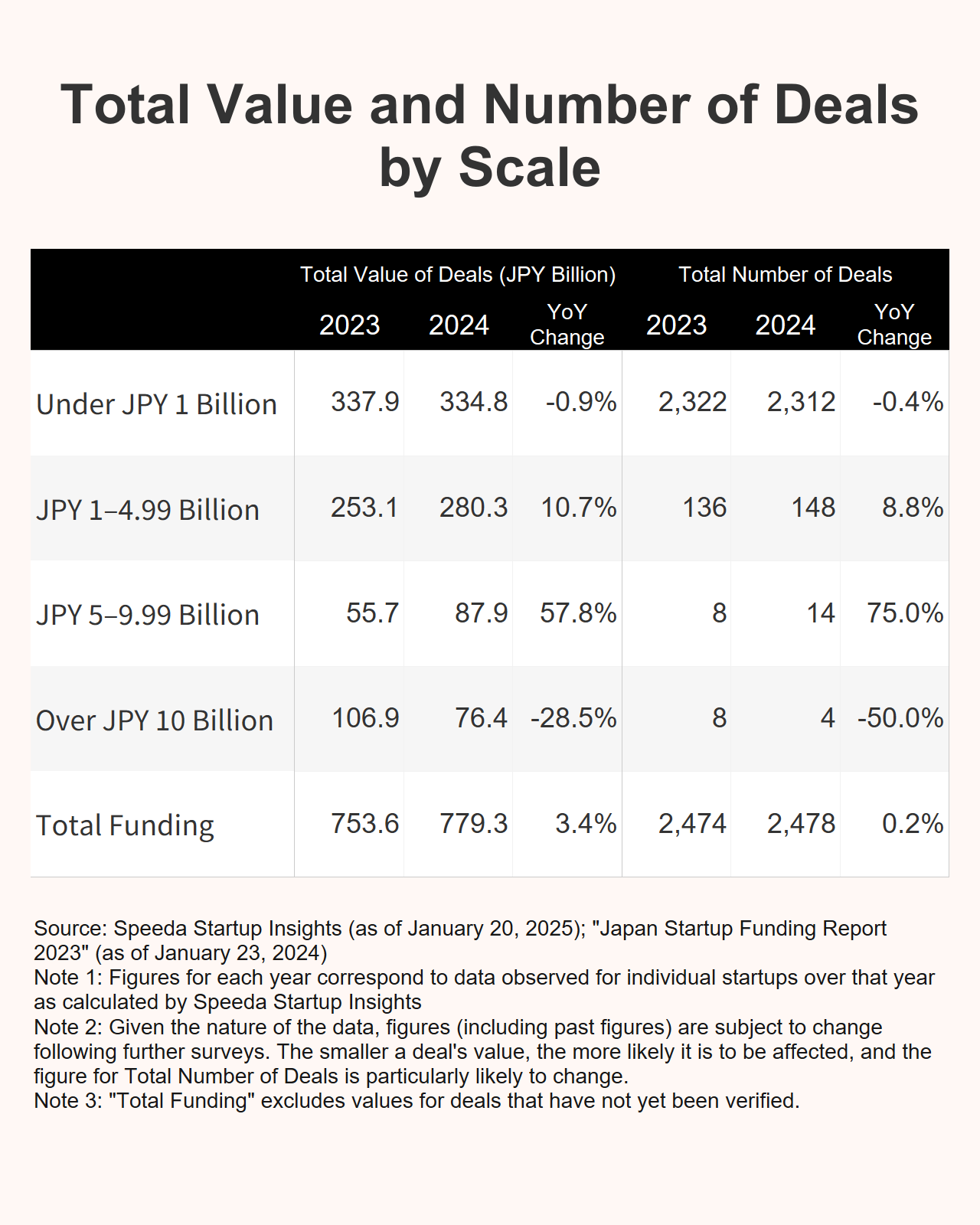

Looking at fundraising by scale, deals between JPY 5 billion and JPY 9.99 billion saw the largest increase in both the number and average value of deals, followed by those between JPY 1 billion and JPY 4.99 billion. While deals of less than JPY 1 billion comprised the bulk of funds raised in H1 2024 (January to June), larger deals were more prominent in the second half of the year, particularly those exceeding JPY 5 billion.

While both the number and average value of deals decreased YoY for deals of JPY 10 billion or more in 2024, both figures exceeded 2023 values when looking at deals of JPY 1 billion or more.

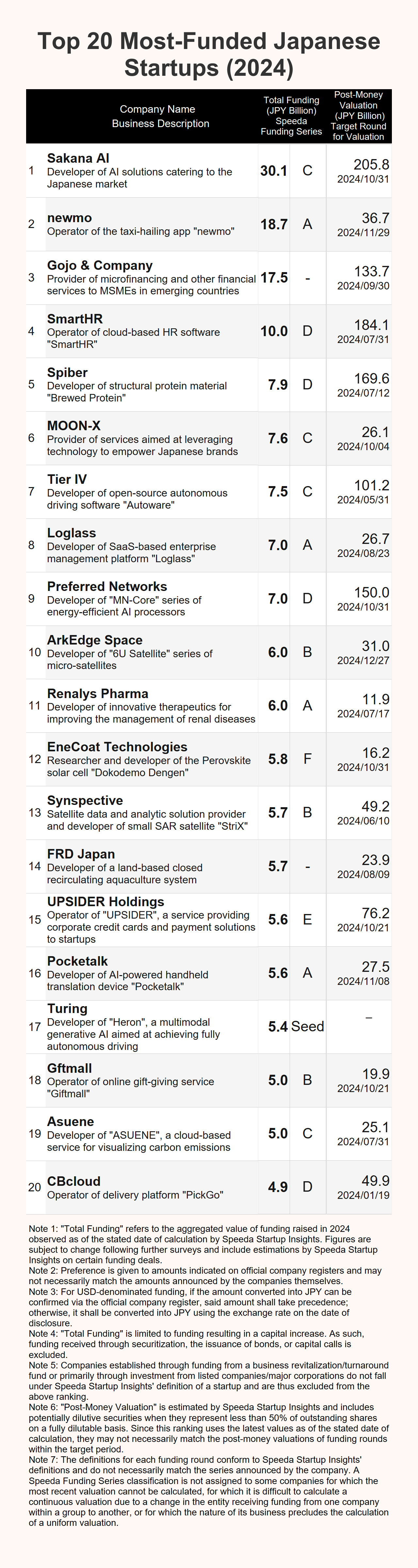

Top 20 Most-Funded Startups

Sakana AI, which raised the largest amount of funding in 2024, became the fastest company to ever reach unicorn status in Japan, with its valuation exceeding JPY 200 billion just over a year after its founding. Started by a team that includes former Google researchers, the company aims to build a world-class AI laboratory in Japan. Although it has received funding from renowned US-based VCs active on the global stage, the company has also received investment from major Japanese players in various fields and is focused on developing solutions to the unique problems facing Japan.

Established in January 2024, newmo raised a total of JPY 18.7 billion in its first year. Founded by Naoki Aoyagi, who had previously served as the head of Mercari's Japanese operations, the company leveraged its fundraising ability to acquire management rights in Kishikou, which operates a taxi business in Osaka Prefecture, and to acquire Miraito, which posted revenue of JPY 5.5 billion in FY2023. As a result of these moves, the company became the fifth-largest taxi operator in Osaka and is currently working to address mobility issues across the country, including launching a domestic rideshare service in July and establishing a subsidiary to lease vehicles for rideshare drivers in August.

Meanwhile, Gojo & Company, which provides microfinancing and other financial services in emerging economies, raised a total of JPY 17.5 billion. In this round, the company took advantage of new fundraising methods such as the J-Ships (JSDA Shares and Investment trusts for Professionals) system for specified investors and publicly offered investment trusts (which began including unlisted shares as a result of a system revision). By diversifying its funding sources and optimising its funding costs in this way, the company aims to achieve sustainable growth.

While the above ranking is compiled using only the amounts indicated on each company’s official register as of the stated date of calculation by Speeda, for reference, Preferred Networks, Terra Charge, and Dinii also issued press releases announcing funding rounds of JPY 19 billion, JPY 10 billion (including debt financing), and JPY 7.5 billion, respectively.

For Preferred Networks, this represented the company’s first equity-based investment since 2019, a year in which its post-money valuation stood at JPY 351.6 billion. As of end-October 2024, however, this figure had fallen to JPY 150 billion, likely a contributing factor to the company’s decision to accept a down round in order to secure funding and ensure its competitiveness amidst intensifying competition for development caused by the generative AI boom.

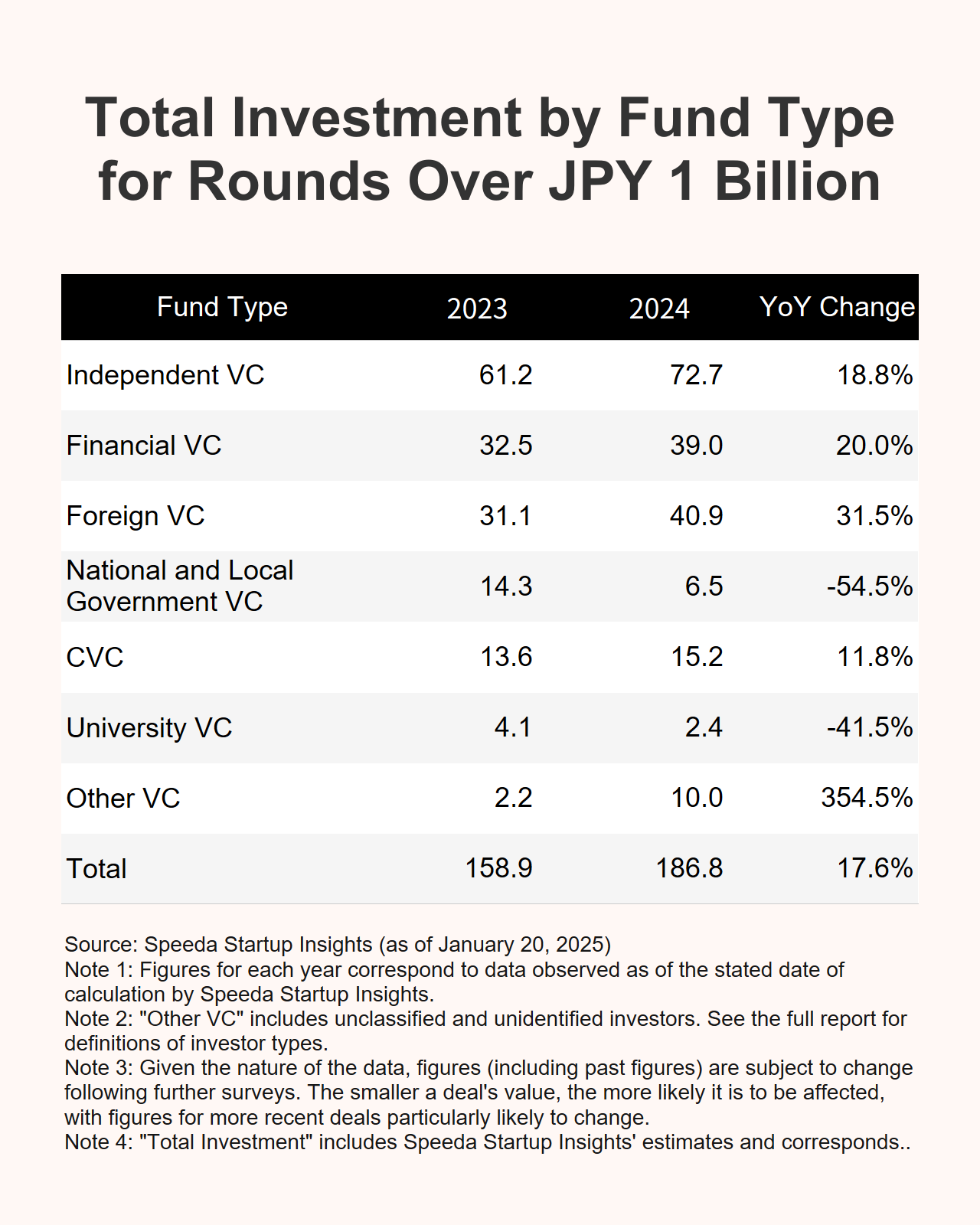

Foreign VCs Making Presence Felt

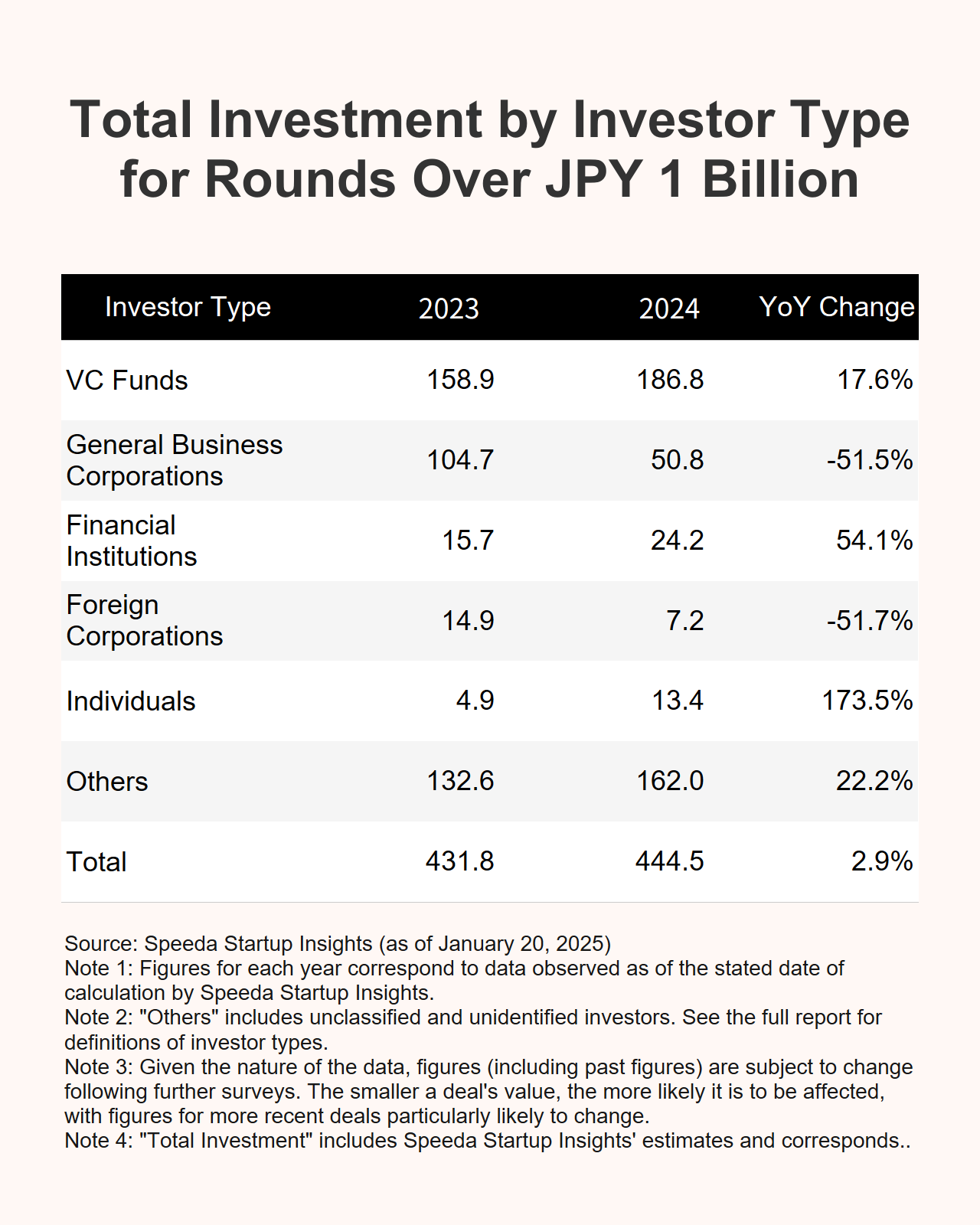

Looking at the types of investors involved in deals valued at JPY 1 billion or more in 2024, of the larger categories, the amount of investment from VC funds rose YoY while direct investment from general business corporations declined sharply. The fact that this category of investors has historically been a stable source of investment for startups makes this change particularly noteworthy.

For reference, secondary transactions (i.e. the sale of shares or stakes in a company by existing shareholders) also increased YoY in 2024, with general business corporations receiving the lion’s share of these transfers at JPY 45.8 billion.

Looking only at venture capital, investment from all funds other than national and local government VCs and university VCs rose in 2024. By category, the increase in funding from foreign VCs was particularly notable, especially when combined with that from independent VCs and financial VCs, which together contributed to offsetting the decrease in funding from national and local government VCs.

Influx of Global Heavyweights

Most of the startups securing large rounds of funding in 2024 were those working on innovative technologies and those looking to go global. This was reflected in the fact that they received financial backing from a broad range of foreign investors in addition to general business corporations and financial institutions in Japan.

Sakana AI, for example, raised funds from top-tier US VCs such as Khosla Ventures, New Enterprise Associates, and Lux Capital. Although their early-stage status excludes them from the above rankings, Habitto and Leaner Technologies received investments from prominent FinTech investor QED Investors and top SaaS investor Bessemer Venture Partners, respectively.

New Enterprise Associates, in particular, has been showing increased interest in the Japanese market since the Japan Investment Corporation (JIC) invested in it as a limited partner in 2023. Meanwhile, as further signs of growing interest in Japanese startups, SmartHR secured rounds of funding from KKR (a major private equity fund) and Teachers' Venture Growth (a Canadian pension fund), while Logras received funding from Sequoia Heritage (a private investment partnership that manages the assets of the management team for US VC fund Sequoia Capital).

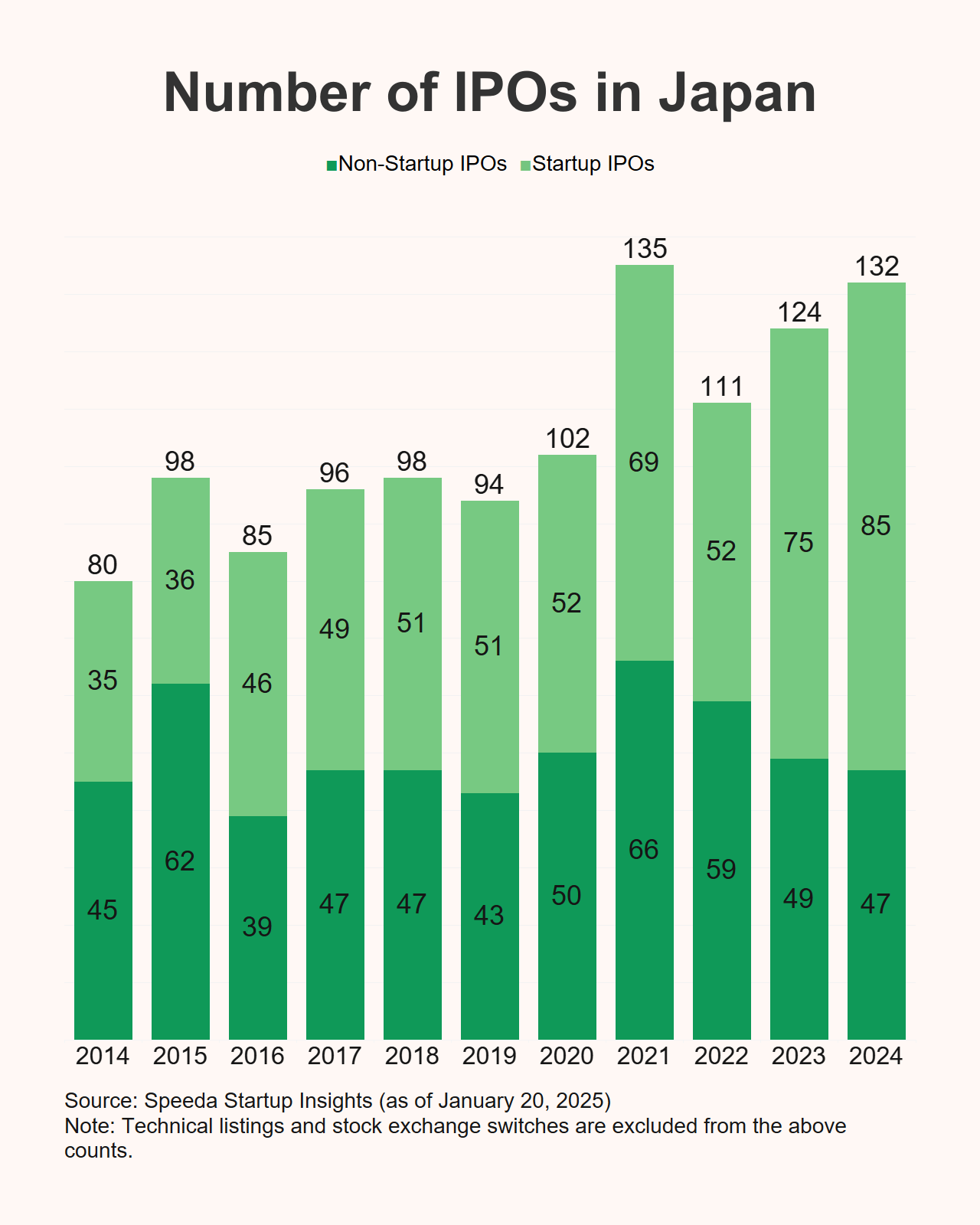

Two Startups Stood Out in Lackluster IPO Environment

While the total number of IPOs in 2024 came close to matching the level of 2021—which was the highest recorded since 2014—at 132, the share of startup IPOs has continued to fall since 2021, totalling just 47. The median market capitalization at the time of IPO for startups was also poor at just JPY 8.9 billion, a considerable drop from the JPY 12.3 billion recorded in 2023.

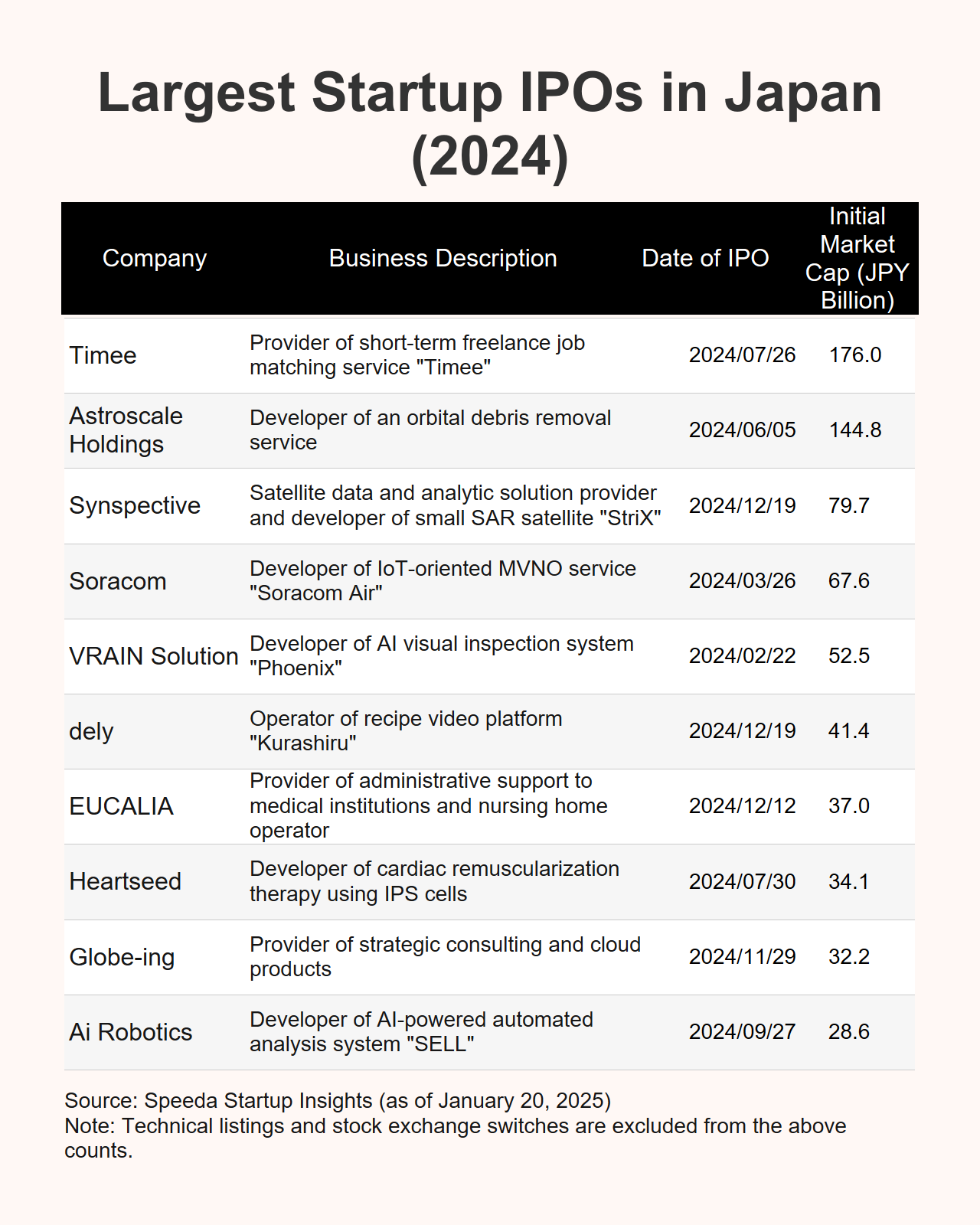

However, two startups still managed to shine, with Timee and Astroscale Holdings each achieving IPOs with an initial market cap of over JPY 100 billion.

Timee has maximised the ability to fill gaps in the part-time job market by matching employers with people seeking short-term work, resulting in revenue of JPY 26.8 billion (+66.5% YoY) and an active account utilisation rate of 86% in FY10/2024.

Before going public, Timee raised funds from independent VCs and invited companies with potential business synergies and foreign institutional investors to become shareholders. In addition to preparing its post-IPO shareholder structure by creating opportunities for secondary transactions, the company also leveraged bank loans. The fact that Timee did not utilise its IPO as a means to raise funds is noteworthy.

In 2024, Japan saw multiple startup IPOs in the space sector, with iQPS, Astroscale Holdings, and Synspective following the lead of ispace, which went public in 2023. The Japanese government has also implemented a national strategy of promoting startups in the space sector, working with the Japan Aerospace Exploration Agency (JAXA) to establish the Space Strategy Fund in 2024, which is set to invest JPY 1 trillion over 10 years in support of space transportation, satellites, and space exploration.

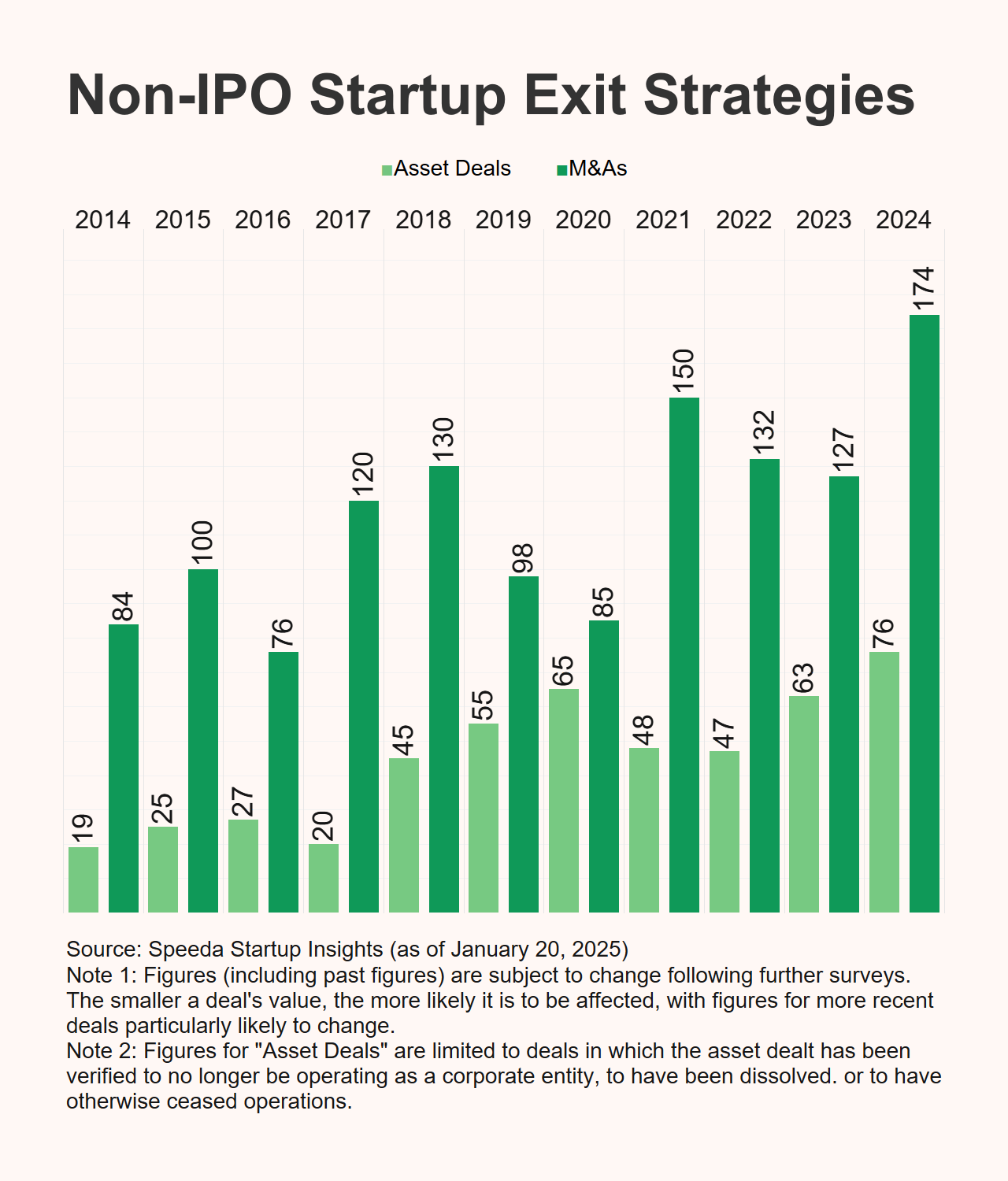

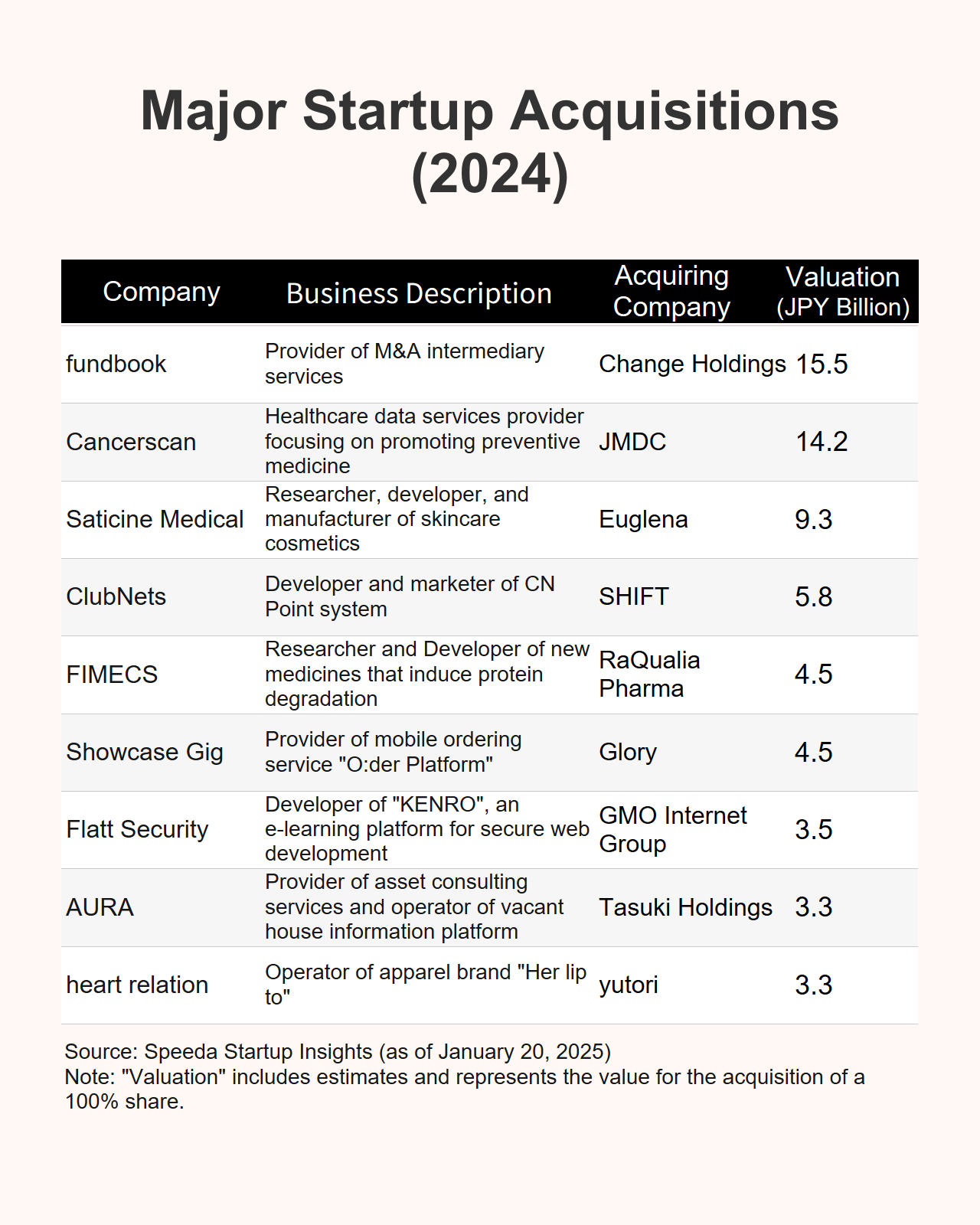

Exit Strategies Diversifying, M&As on the Rise

Both M&As and asset deals were up in 2024, with the increase being particularly notable in the former, reaching their highest level since 2014. Meanwhile, the median number of years from founding to acquisition was 7.8 years, also the longest since 2014.

Of the major M&A deals seen in 2024, those involving conditions other than a 100% acquisition of the startup’s assets featured prominently. An increasing number of deals have begun to feature flexible schemes such as the gradual acquisition of shares in accordance with post-acquisition performance and the retention of independent management through partial shareholding by pre-acquisition management teams. One factor contributing to this phenomenon could be that, in addition to large corporations, former startups that have since listed on the TSE Growth Market have also been making more acquisitions.

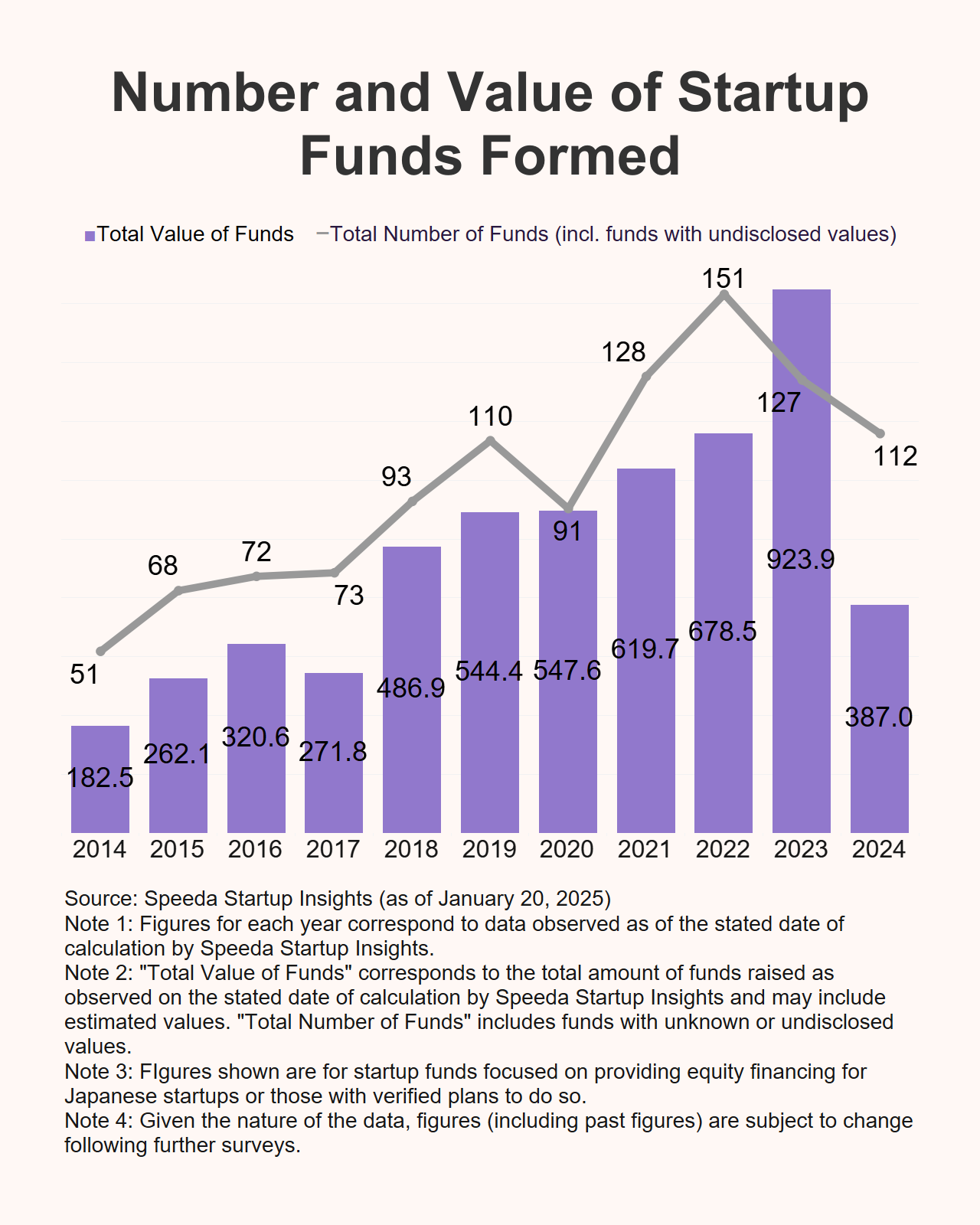

Tide Could be Turning for New Funds

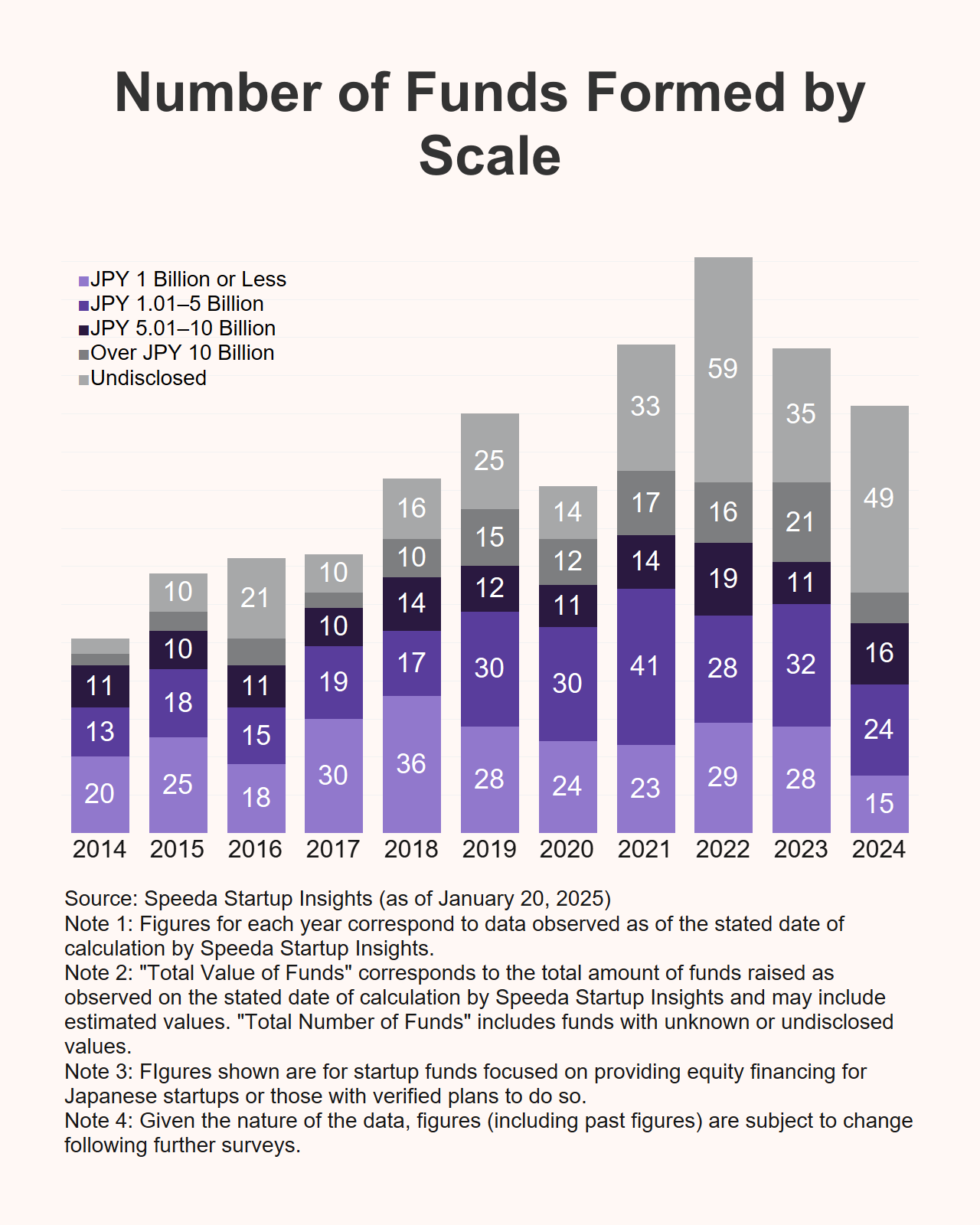

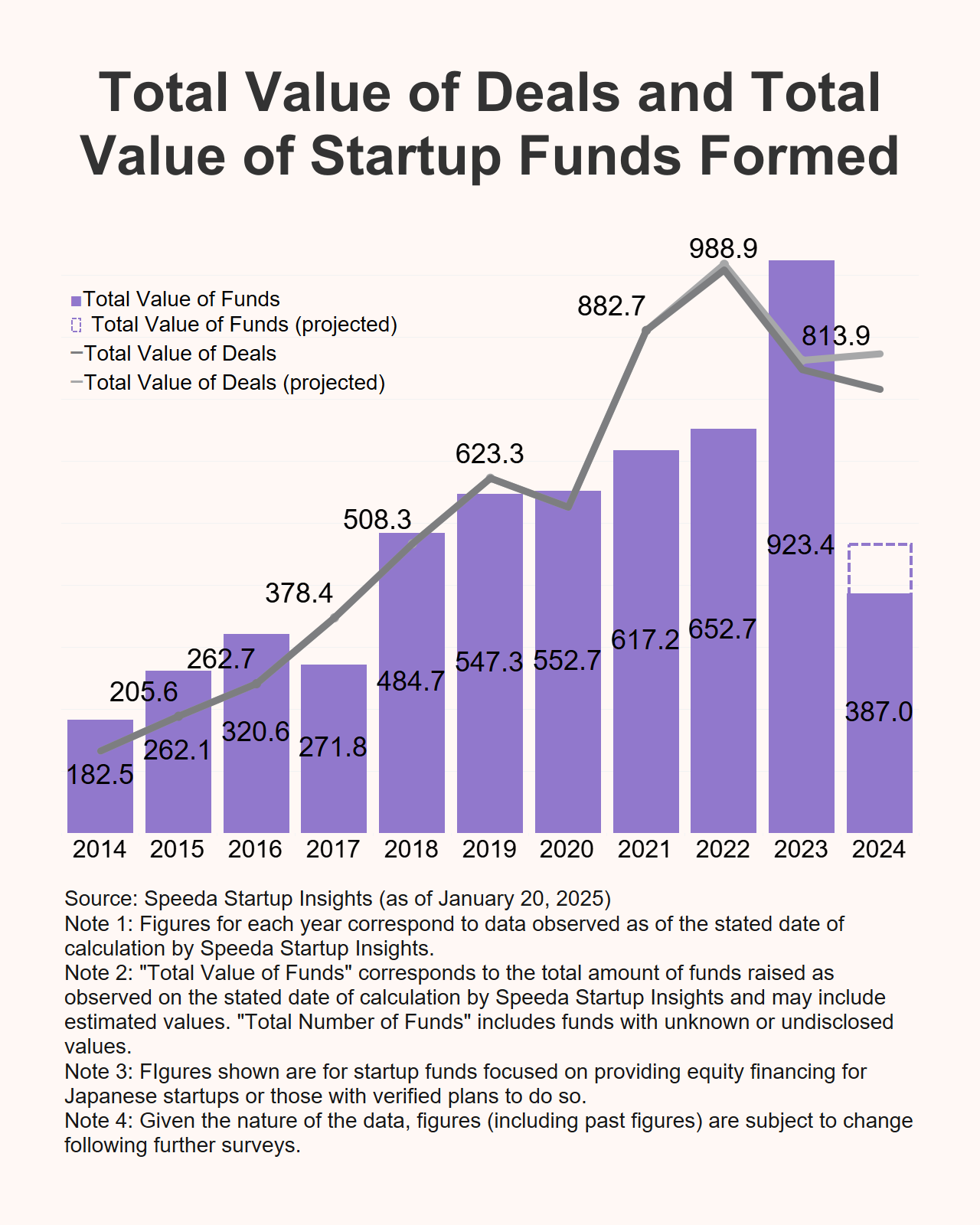

In 2024, 112 new startup funds were formed with a total combined value of JPY 387 billion.

Although both of these figures represented YoY declines, the decrease in the latter was particularly sharp and marked the reverse of a decade-long trend. Of course, this figure may rise as data on more funds is released. However, even when accounting for such cases, the total combined value of funds formed in 2024 is unlikely to surpass the level recorded in 2018. It should also be noted that the figure for 2023 in the following chart appears particularly striking due to the inclusion of the Japanese government-backed JIC Venture Growth Fund No. 2 (valued at JPY 200 billion)—which had been recorded as part of the total for 2022 in previous editions of this report—after it was newly discovered to have, in fact, been founded in 2023.

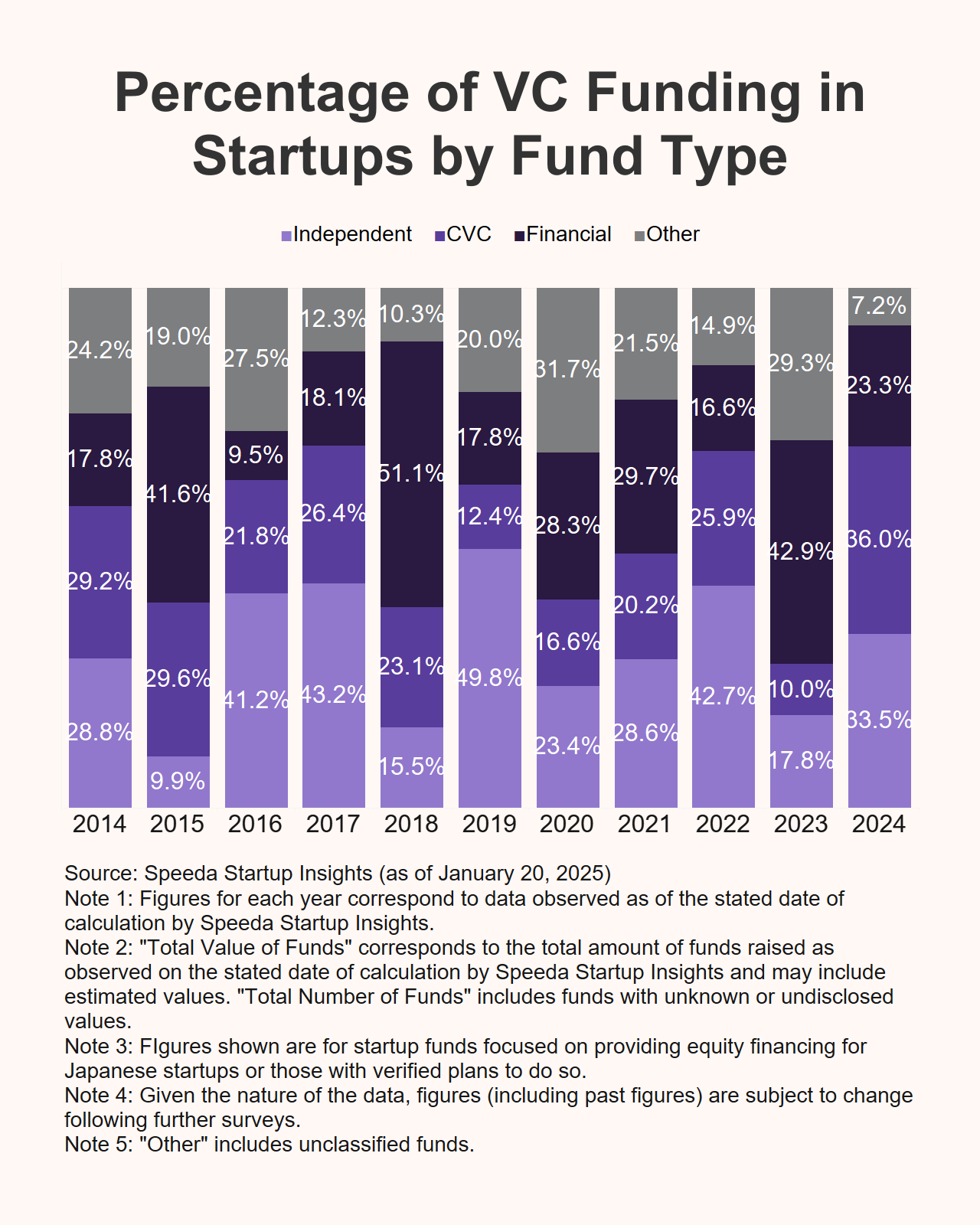

By type, the percentage of funding in startups from CVCs increased in 2024. Of particular note is that while the number of these funds decreased by three YoY, their combined value actually increased.

At the same time, this suggests that the overall decrease in the number of funds formed in 2024 was largely attributable to a reduction in the number of funds backed by financial institutions.

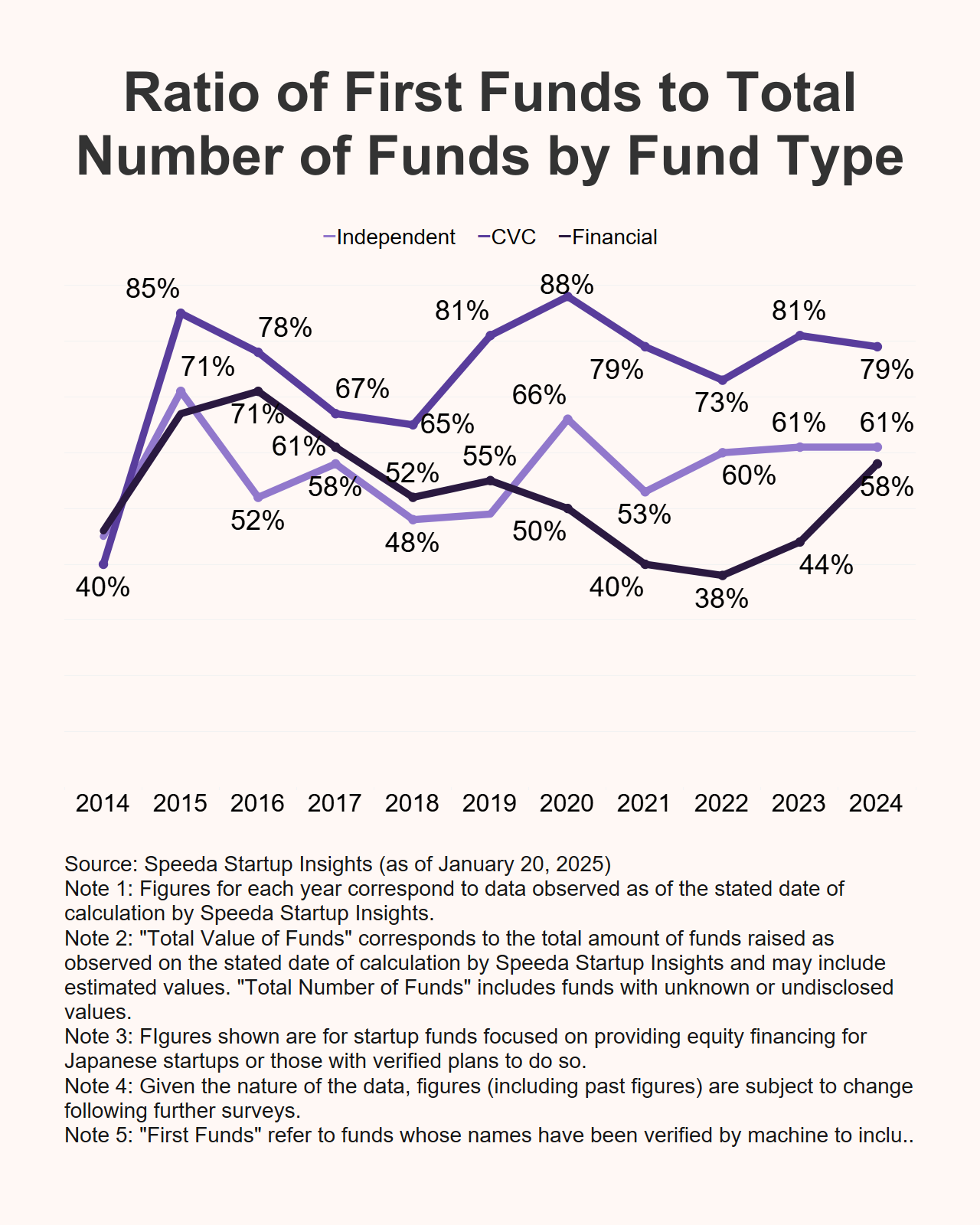

The only types of fund to see an increase in the ratio of its first funds to the total number of funds were those backed by financial institutions.

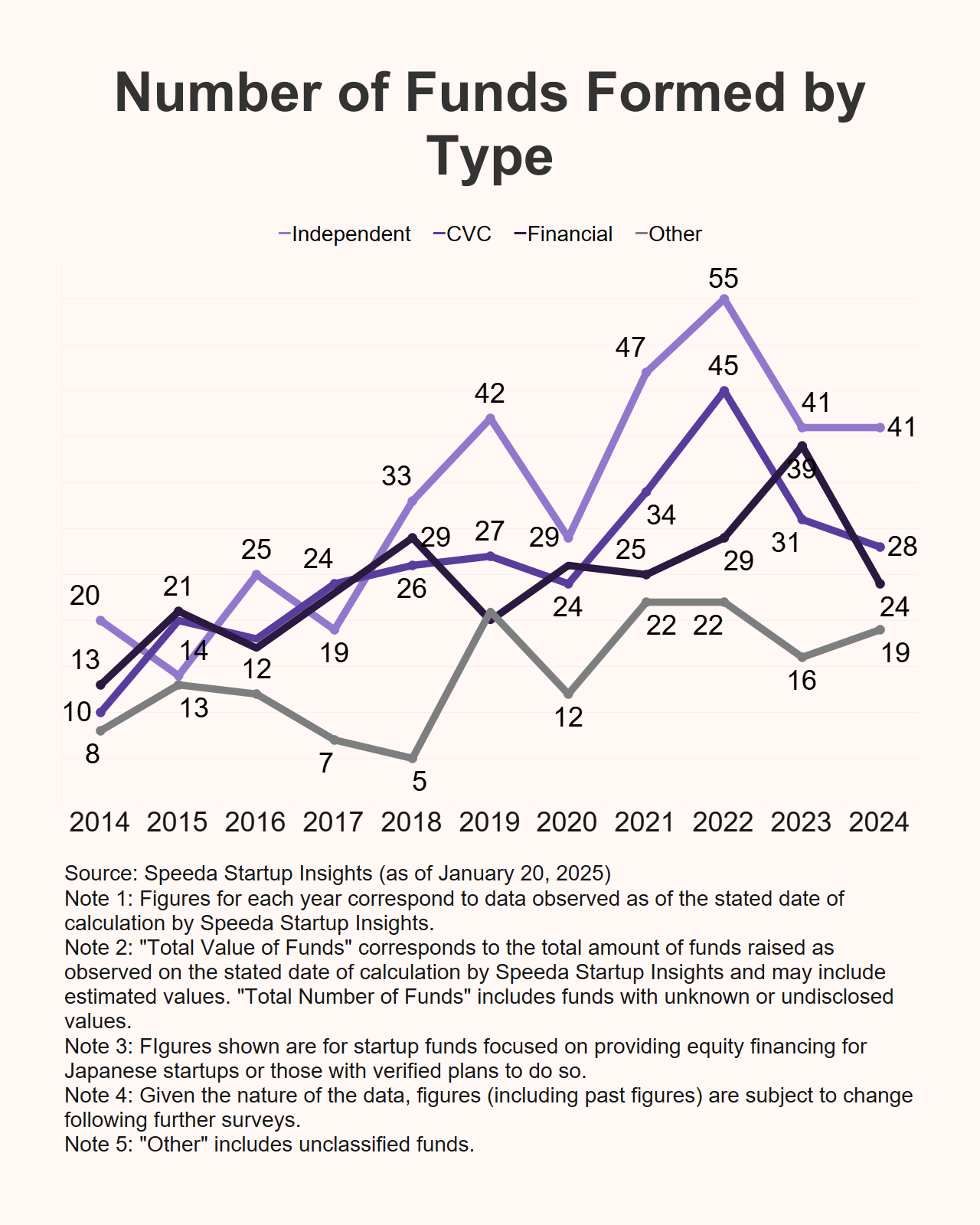

Meanwhile, the average value of a startup fund in 2024 stood at JPY 6.1 billion, well below the JPY 10 billion recorded in 2023. This was likely due in large part to the number of funds valued at over JPY 10 billion falling from 21 to 8 over 2023–24.

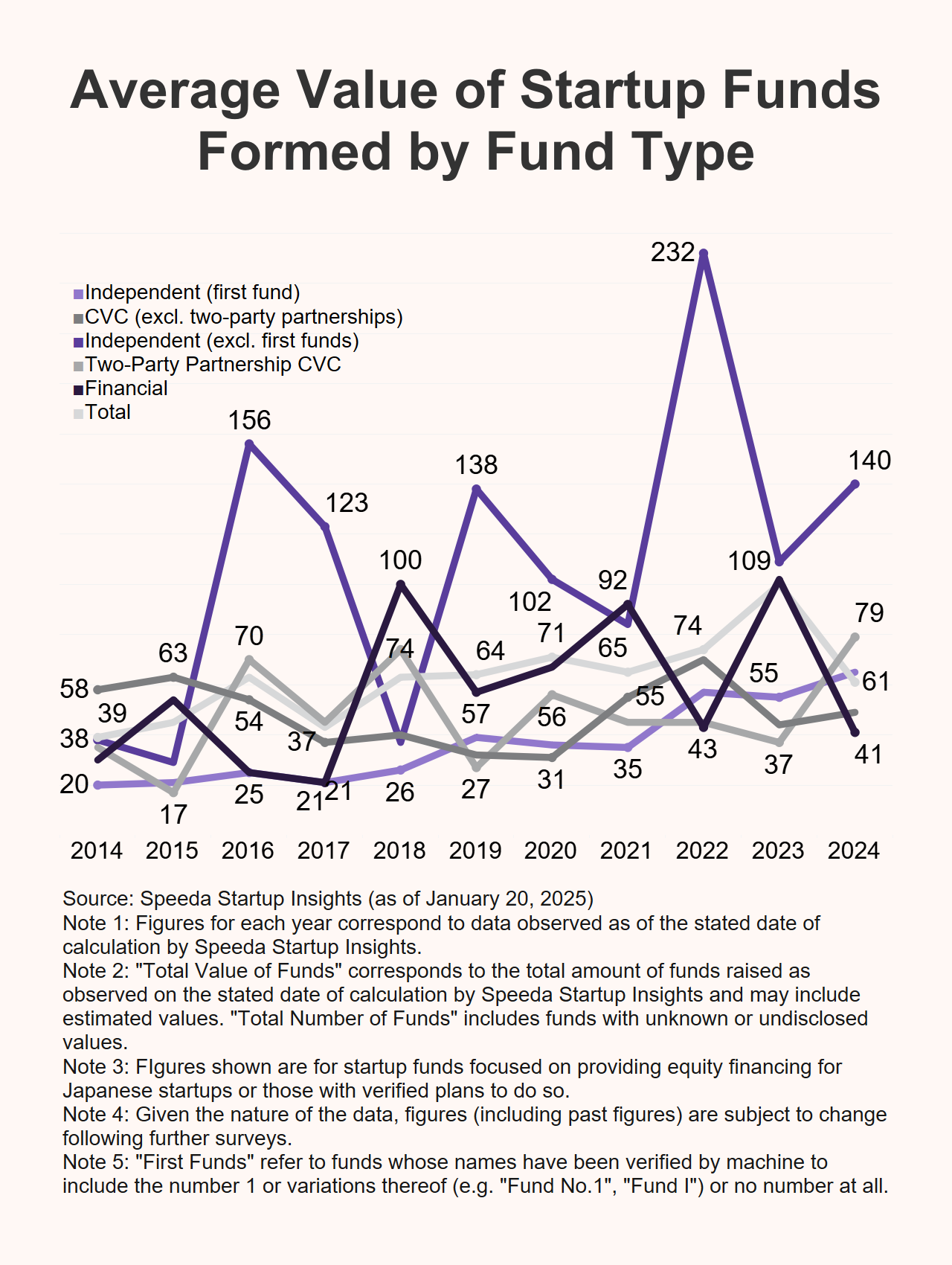

However, the average value of a startup fund has increased for independent funds—particularly when first funds are excluded—and for two-party partnership CVCs.

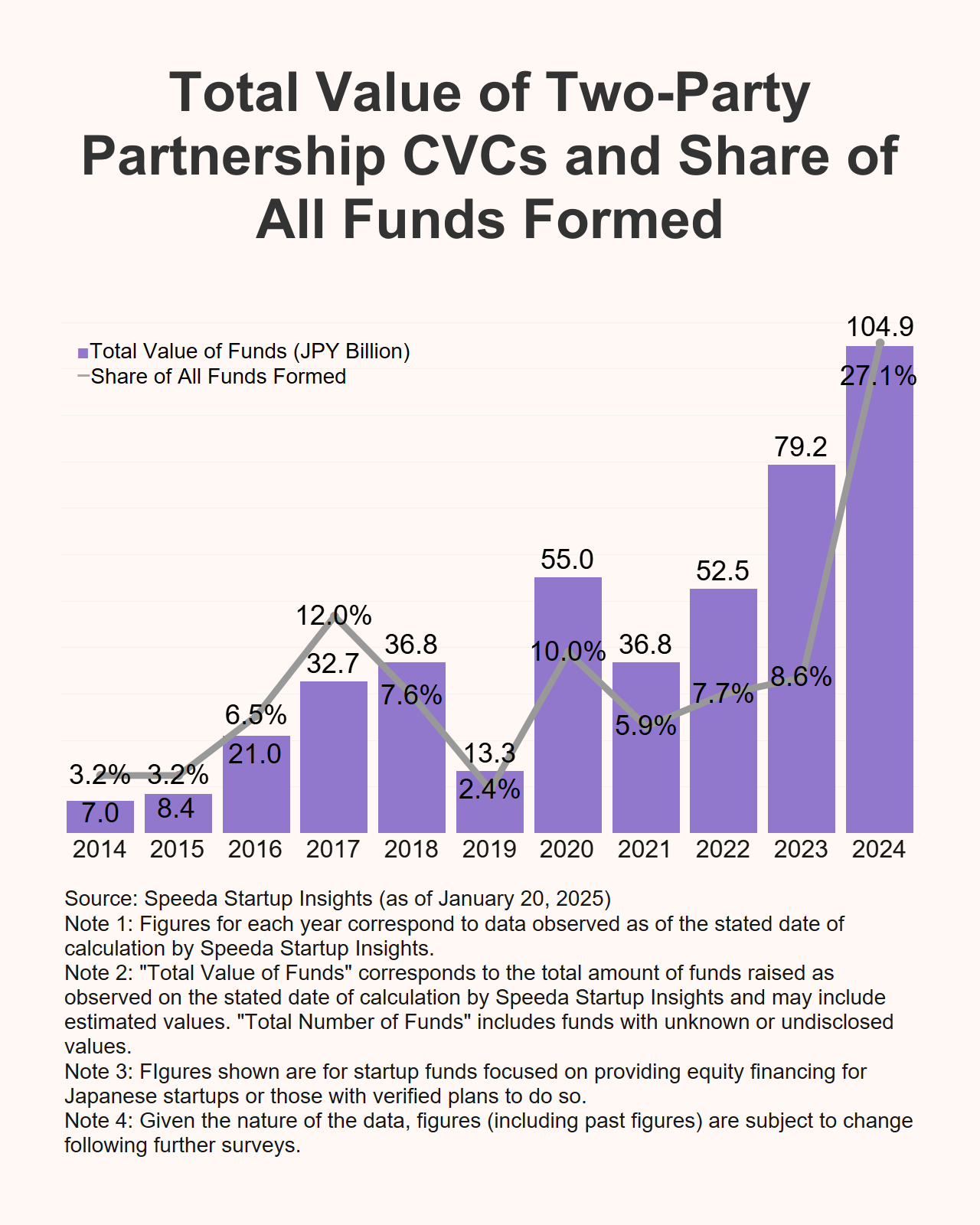

The formation of two-party partnership CVCs has become increasingly common since 2021. As of 2024, two-party partnership CVCs comprised half of all CVCs formed and accounted for 27% of the total value of all funds formed that year with a combined value of JPY 104.9 billion.

Looking at the relationship between the amount of funding raised by startups and the combined value of startup funds formed in a given year, the total value of all deals secured by startups generally increased in line with the rise in the total value of funds through 2019. However, these two figures diverged sharply over 2021–22 due to expanded direct investment from general business corporations and the substantial impact of an influx of foreign capital.

While it is possible that the decline in the total value of funds formed in 2024 may ultimately end up encumbering fundraising efforts from H2 2025 onward, considering the slowdown in the pace of investment since 2022 and the fact that investors have a fair amount of dry powder on hand, it could be some time before this impact becomes evident.

Final Thoughts

The year 2024 was characterised by two conflicting trends: an influx in funding from foreign investors and a decrease in the total value of funds formed. Despite a decline in direct investment from general business corporations, Japanese startups nonetheless remained an attractive investment target, as evidenced by an increase in the number of CVCs formed and the increased frequency of secondary transactions and M&As.

Going forward, players in Japan’s startup ecosystem will need to keep an eye on three indicators: 1) how many VC funds are being formed, 2) the level of involvement from general business corporations, and 3) how much capital is flowing in from foreign investors. The IPO environment and trends in government support will also be important factors to consider.

For its part, the Japanese government is supporting globalisation and the creation of deep tech startups, with a focus on fostering human resources and incubation networks and strengthening funding and diversifying exit strategies for those companies. Looking to capitalize on the events scheduled to be held from April at Expo 2025 in Osaka, the government is planning to increase its efforts to attract foreign investors and ramp up the promotion of its Startup Development Five-Year Plan.

Although investors may take on a more discerning approach, backing from the Japanese government is likely to open doors for deep tech companies with solid technological capabilities and other competitive startups in the country to secure large rounds of funding.

Text: Atsuko Mori, Ryo Hirakawa

Editing: Atsuko Mori

Design: Nanami Kawasaki

Illustrations: noa1008

English Version: Cody Branscum, Laura Wakefield